Your biggest cost is the one nobody talks about

Asset management in social and affordable housing is broken. Here is why that matters and what needs to change.

HUD’s Flexible Fund and 25‑year contracting model assume CHPs will operate a “whole‑of‑life” asset management system aligned with ISO. But for the vast majority of CHPS governance, development, tenancy management and maintenance are frequently siloed. No one role is clearly accountable for portfolio health over decades. When revenue constraints add further pressure when rental income struggles to cover rising costs, it is tempting to defer big renewals to make the operating budget balance. That can quietly turn into a backlog that future boards inherit.

Now imagine running a bus company but only ever budgeting for fuel and tyres, never engine rebuilds or eventual replacement; it might work for a while, but one day the fleet simply fails. That is where a number of CHPs risk ending up with their housing stock.

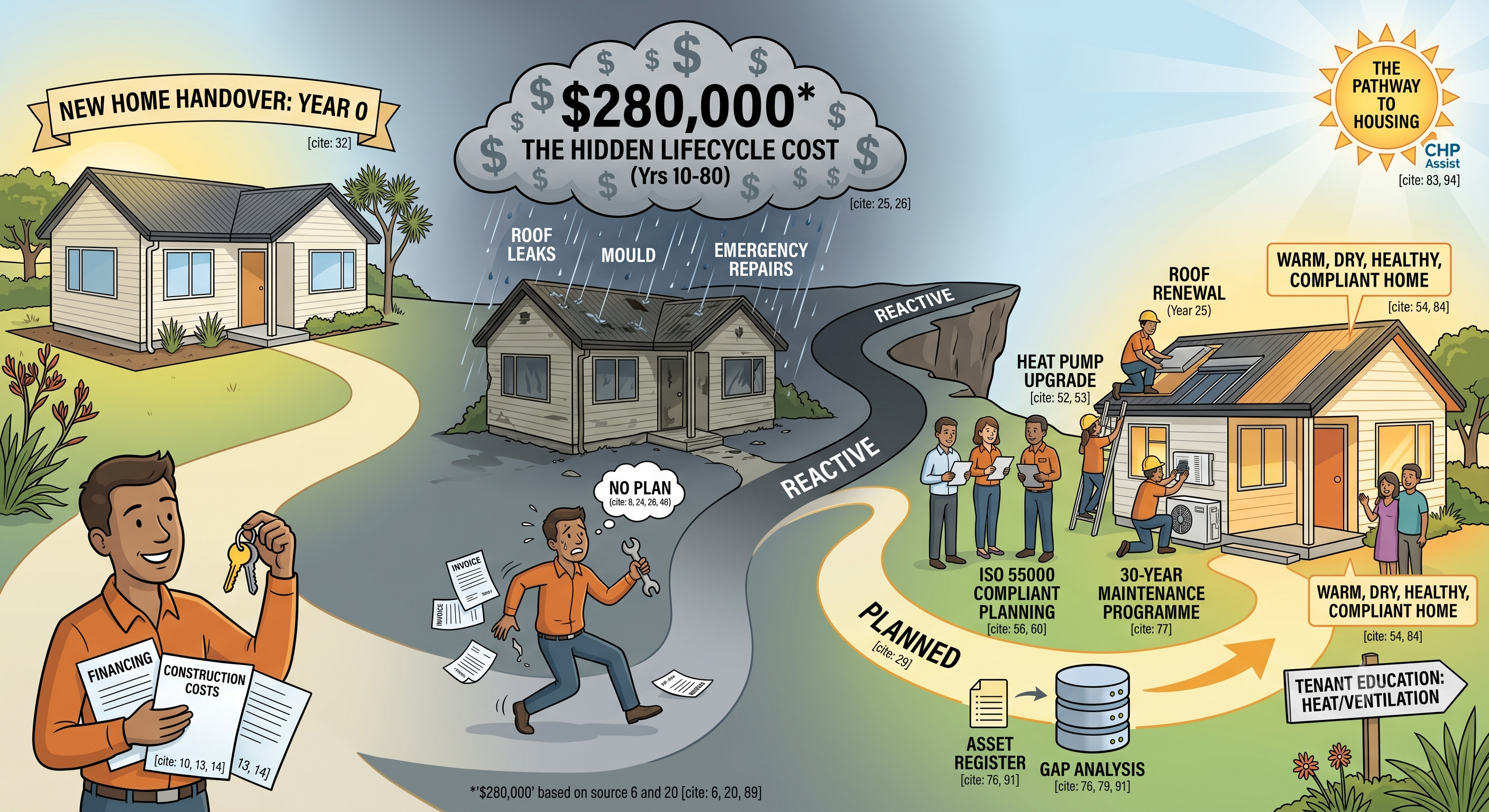

Let us start with a number: $280,000.

That is the estimated cost to maintain one average dwelling over 70 years from years 10 onwards. In today's money.

Most CHPs do not have a plan for that number. Many do not even know it exists.

That should concern all of us.

The financing gets all the attention. The asset costs get ignored. But they will arrive whether you are ready or not.

The cost hiding in plain sight

Many CHPs still treat “development” or “acquistion” as the project and “asset management” as an afterthought or a compliance cost. Homes are acquired, tenanted and maintained, but not consistently planned over their full lifecycle from creation to disposal/redevelopment.

This shows up as:

· Reactive maintenance rather than planned programmes.

· Minimal long‑term provision for renewals and upgrades.

Weak links between organisational strategy, financial planning and asset decisions

A systems approach to the lifecycle ownership of housing stock through strategic asset management which is the lengtheist and most intensive phase of the lifecycle for a CHP (Sharam, A., McNelis, S., Cho, H., Logan, C., Burke, T. and Rossini, P. (2021) https://www.ahuri.edu.au/research/final-reports/367)

Most CHPs rightly focus their energy, time and capabilities acquiring properties for their portfolio. But few think about the long-term implications and demands of managing a growing portfolio. Yet once a home is in the portfolio, the real cost of property ownership begins.

Asset management is everything that keeps that home fit to live in. It covers routine repairs and maintenance. It also covers planned capital replacements, sometimes called renewals. Think roofs, kitchens, bathrooms, heating systems, insulation, cladding, windows and structural work.

These are not optional extras. They are the obligations that come with ownership.

And across a typical 70-year lifespan, they add up to around $280,000 for an average dwelling ($4,000 over 70 years). In today's value.

That figure is largely invisible in the social housing sector in New Zealand.

The sector has a planning problem

Here is what we see in practice. Community housing providers (CHPs) sit on portfolios worth many millions, yet many are still forced to think in 3-5 year financing cycles rather than 50-70 year asset lives. That gap between long‑life assets and short‑term thinking is at the heart of the sector’s planning problem.

This means most CHPs only start thinking about asset management when something breaks. A roof starts leaking. A hot water cylinder fails. Mould becomes a complaint. A Healthy Homes inspection flags issues.

Then the scramble begins. Emergency repairs. Insurance claims. Tenant disruption. Unfunded costs.

This is reactive management. It is expensive. It damages relationships with tenants. It creates risk for the organisation and at worst threatens the CHP’s HUD funding.

And it is completely avoidable.

Reactive asset management costs more than planned maintenance. Every time.

The problem starts at governance

This is the uncomfortable truth the sector needs to hear. Most boards can recount their last development deal in detail – land, consents, funding, ribbon‑cutting. Far fewer can pull out a simple view of how that new stock will be maintained, renewed and eventually replaced over its full life, and how that is funded

By the time a building is handed over, nearly all of the big decisions are already made. But governance, development and operations are often split, so no single decision‑maker is accountable for lifecycle performance of the portfolio.

On top of that, constrained revenue (income‑related rents / affordable rent contributions) makes it tempting to defer major works to “make the numbers work”, even though this just stores up bigger costs and risks later.

In short: the sector often owns homes, but does not always “steward” them as 50–70 year social infrastructure.

In reality this inability to play a stewarding role over the portfolio leads to practical and costly errors: The wrong roof type is set. A cheap but leaky cladding is installed. The heating system is chosen. If those choices were poor ones, the maintenance burden is locked in for decades. The result is that CHPs can end up owning properties with a maintenance liability they did not fully price in.

Stewardship, or asset management thinking needs to first happen at the board level, which will eventually filter down to the rest of the organisation to the design and planning stage. Not after handover. Then the real questions will start to be asked: What is the expected life of each component? What does replacement cost? When will it fall due?

These questions should be part of every feasibility. Every consent application. Every funding submission.

Right now, they often are not.

Consequences we’re already seeing

Where lifecycle planning is weak, the sector sees:

· Increasing maintenance backlogs and properties hovering near the minimum standard.

· Occasional “surprise” write‑offs or sales of run‑down homes, often at the worst possible time in the market.

· Under‑investment in things like energy efficiency, accessibility and climate resilience, despite clear long‑term benefits and emerging funder expectations.

To compound matters for CHPs, HUD (soon to merged into the Ministry of Cities, Environment, Regions and Transport- MCERT) has reporting requirements related to asset management. The Community Housing Regulatory Authority (CHRA) has governance expectations. Funders like MCERT now require an Asset Management Plan as part of Flexi-Fund contracts. Yet at CHP Assist we know many CHPs including those that have applied for Flexi-fund contracts recently either face the scenarios listed above and/or do not have an MCERT-compliant asset management plan that would unlock the funding they require.

You cannot plan for costs you have not modelled. And most of the sector has not modelled this.

What good looks like

For boards and operational leaders, “good” asset management is about a clear, joined‑up story from mission to money to maintenance.

It starts with a visible line of sight from your purpose (who you house, where, and to what standard) through your portfolio strategy (where you grow, hold, redevelop or exit) into concrete asset plans that set what work is done, when, and why. “Good” also means lifecycle‑based planning (development/acquisition, management, disposal/redevelopment) instead of reactive “fix when broken”, using simple but reliable data on condition, demand and risk to programme renewals and redevelopments.

You do not need a gold‑plated system, but you do need a clean asset register, repeatable condition assessments, basic dashboards the board can read, and governance with enough asset literacy to challenge short‑term decisions that harm long‑term portfolio health. A well-maintained older home tells a different story. Walk through a property that has been planned and maintained properly. The roof was replaced at year 40. The kitchen was renewed at year 15 & 30. The heat pump was upgraded. The insulation meets current standards. The home is warm. It is dry. Tenants are healthy. There are no emergency calls. That outcome does not happen by accident. It happens because someone did the planning early and followed through.

Finally, Good practice starts with integrating asset and financial planning, so MCERT subsidies, tenant rents, upfront funding and debt are all deliberately tied to the cost of long‑term renewals and upgrades. At the same time, tenants stay at the centre of every decision, with boards consciously balancing financial optimisation against stability, wellbeing and levels of service. ISO 55000, the international asset management standard, sets the benchmark for this. It calls for a whole‑of‑life approach to assets and expects organisations to keep an up‑to‑date Asset Management Plan, not a static document that is revisited every few years.

In Aotearoa, this expectation is now embedded in contracts: MCERT’s new Flexi‑Fund terms (clauses 5.1–5.4) require CHPs to maintain an asset management system and to operate in line with a current plan at all times. That is not an unreasonable bar; it is simply the standard for any organisation entrusted with long‑lived social infrastructure, and our sector needs to consistently meet it.

Does your CHP have an asset management plan that conforms with ISO 55000?

Tenancy management plays a bigger role than people realise

Here is one more area that gets overlooked.

Asset management is not just about buildings. It is also about how people live in them.

A tenant who does not know how to use the ventilation system creates condensation and mould.

A household that cannot afford to run the heat pump leaves the home cold and damp.

That accelerates wear and tear. It creates health problems. It generates maintenance call-outs.

Good tenancy management includes educating whanau about ventilation and heating. It connects them to support if energy costs are a barrier.

That is not a soft outcome. It reduces maintenance costs. It reduces preventable medical events. It keeps homes in better condition for longer.

The link between tenancy management and asset condition is real. Very few CHPs manage it as one system.

The home is warm when the people in it know how to keep it warm. That is a management task, not just a building task.

What CHPs can do right now

This does not have to be overwhelming. It starts with knowing what you have. You can use the following questions to take a quick stock-take:

· Do we have a current asset management policy, strategy and plan, and has the board discussed them in the last 12 months?

· Does our asset register fulfil the requirements of the stewardship approach to owning social housing and/or affordable homes?

· Can we see, at portfolio level, our planned renewals, upgrades and redevelopment over at least 10 years, and how these are funded?

· Do our regular board reports include simple “portfolio health” information, not just arrears and vacancies?

· Are tenant outcomes and feedback visible in major asset decisions?

If not, the planning problem is probably alive in your organisation – and now is the time to treat asset management as core governance work, not a technical back‑office function.

That gap analysis is critical. It tells you what you are carrying. It helps you make the case to funders. It supports board decision-making.

It also protects your tenants. Because the alternative, deferring maintenance until things fail, falls hardest on the people living in the homes.

You do not need an expensive system to start

Many CHPs hear "asset management" and think software. They picture expensive platforms, long implementation projects, and consultants charging by the hour.

That is not where you need to start.

A well-structured spreadsheet is enough for most early-stage portfolios. It does not need to be sophisticated. It needs to be consistent.

Record each property. List every major component. Note the age, the expected life, and the likely replacement cost. Update it when work is done.

That is an asset register. It is the foundation of everything else.

From there you can build a simple renewals schedule. Flag what is due in the next five years. Estimate the cost. Start setting money aside.

That is an Asset Management Plan. It does not need to be 80 pages to be useful.

The goal at the start is visibility. What do you have? What is its condition? What is coming?

A spreadsheet gives you that. And it costs nothing.

CHP Assist can create this for you and provide the support to ensure its fit for your needs.

How CHP Assist can help

CHP Assist brings 40 years of lived experience in community housing asset management in New Zealand.

We work with CHPs to build Strategic and Operational Asset Management Plans that are practical, fundable and compliant with MCERT requirements.

We can provide a gap analysis between your existing stock and your planned level of service.

We understand the funding environment. We understand the regulatory framework. And we understand the realities of running housing on thin margins.

If your organisation does not yet have a credible long-term asset management plan, now is the time to start.

The $280,000 is coming. The question is - are you ready for it.

Want to know where your portfolio stands?

CHP Assist offers a gap analysis of your existing stock against your planned level of service.

Contact Guy Brocklehurst: info@chpassist.com | 021 703 511

www.chpassist.com